The Hidden Price Tag of AI

The Hidden Price Tag of AI

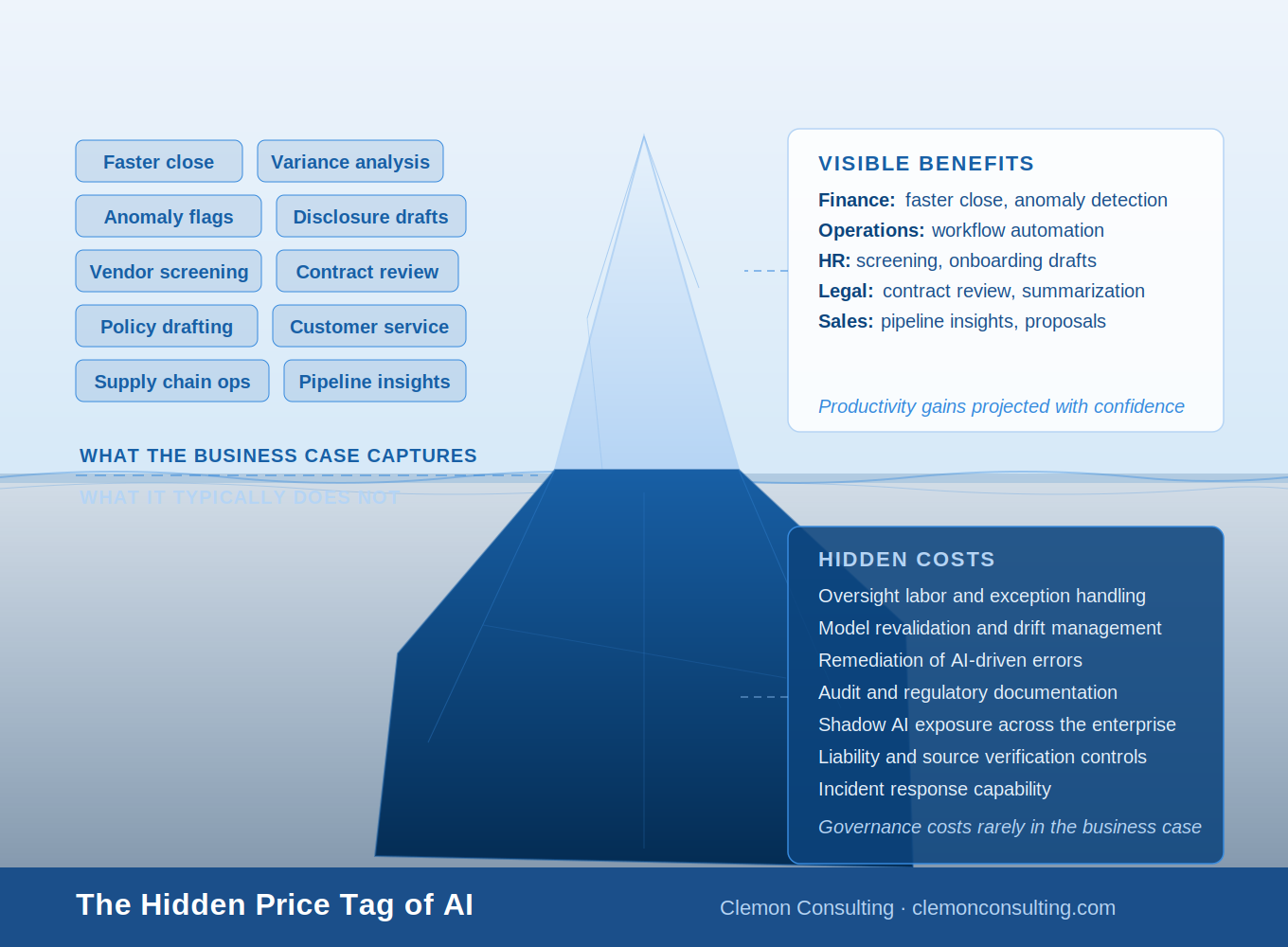

Every AI business case captures the efficiency gains with care and the governance costs with optimism. That asymmetry is where implementations go wrong.

Artificial intelligence is being adopted across finance, accounting, and enterprise operations at a pace that has outrun the governance frameworks designed to keep it in check. The productivity story is real. But every efficiency gain sits alongside a risk that rarely appears in the business case: oversight labor, model revalidation, remediation costs, audit documentation, and liability exposure that can dwarf the license fee.

The organizations that navigate AI adoption well are not those that move fastest. They are those that treat governance, human oversight, and control design as core inputs to the investment decision, not afterthoughts.

Read our full blog post for the key risks, the human-in-the-loop framework, and what it means when AI does not know it is wrong.

Key Changes to Disaggregated Financial Reporting, with Practical Examples: Understanding ASC 220-40

ASC 220-40 marks a meaningful shift in financial reporting, requiring companies to move beyond high-level expense categories and provide a more transparent view into what’s really driving their cost structure. Where financial statements once grouped expenses into broad buckets like cost of goods sold or SG&A, stakeholders will now expect a clearer breakdown of underlying components such as labor, materials, depreciation, and other key inputs.

This change is not just about compliance—it’s about clarity. Investors, lenders, and operators alike benefit from a more detailed understanding of how a business allocates its resources and where margin pressure or efficiency gains truly exist. For many organizations, ASC 220-40 will surface insights that were previously buried in aggregated reporting, ultimately leading to better decision-making and more informed conversations around performance.

As companies prepare for adoption, those that take a proactive approach—aligning systems, refining their chart of accounts, and enhancing internal reporting—will be best positioned to turn this new standard into a strategic advantage rather than a last-minute reporting exercise.